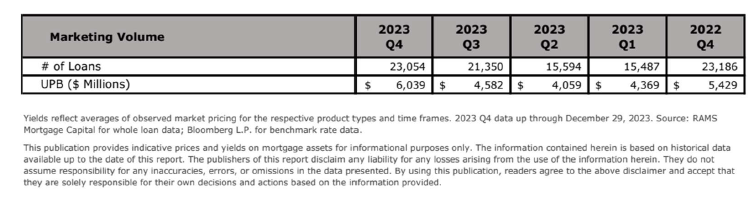

This publication provides indicative prices and yields on mortgage assets for informational purposes only. The information contained herein is based on historical data available up to the date of this report. The publishers of this report disclaim any liability for any losses arising from the use of the information herein. They do not assume responsibility for any inaccuracies, errors, or omissions in the data presented. By using this publication, readers agree to the above disclaimer and accept that they are solely responsible for their own decisions and actions based on the information provided.

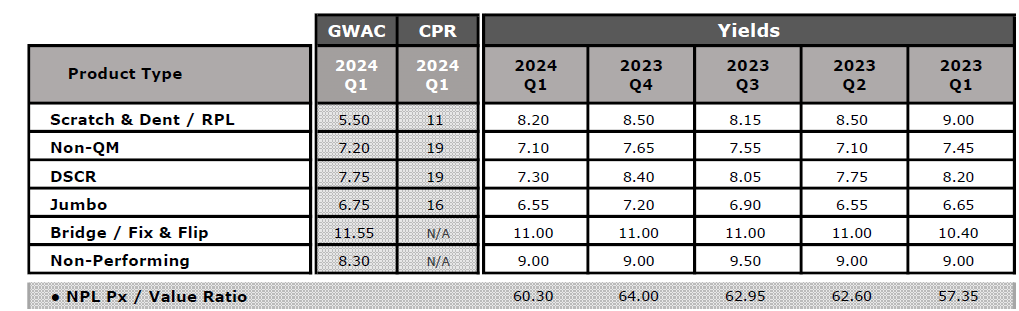

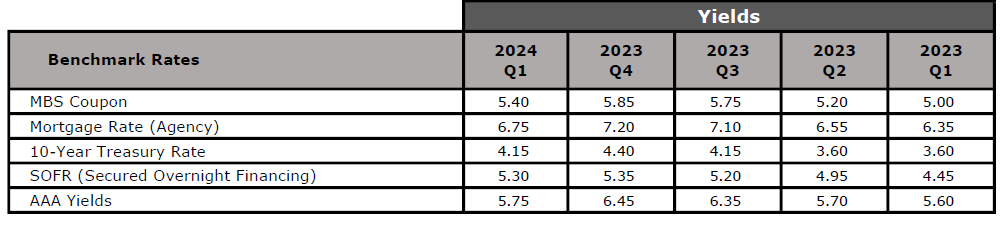

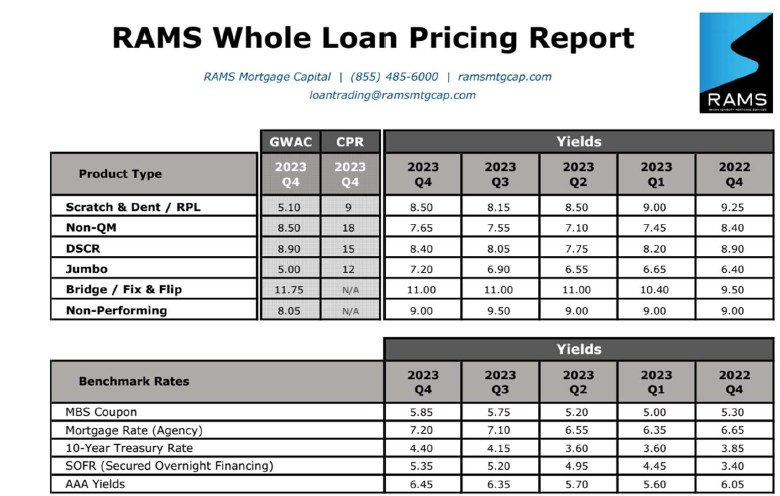

Yields reflect averages of observed market pricing for the respective product types and time frames. 2024 Q1 data up through March 29, 2023. Source: RAMS Mortgage Capital for whole loan data; Bloomberg L.P. for benchmark rate data.

This publication provides indicative prices and yields on mortgage assets for informational purposes only. The information contained herein is based on historical data available up to the date of this report. The publishers of this report disclaim any liability for any losses arising from the use of the information herein. They do not assume responsibility for any inaccuracies, errors, or omissions in the data presented. By using this publication, readers agree to the above disclaimer and accept that they are solely responsible for their own decisions and actions based on the information provided.

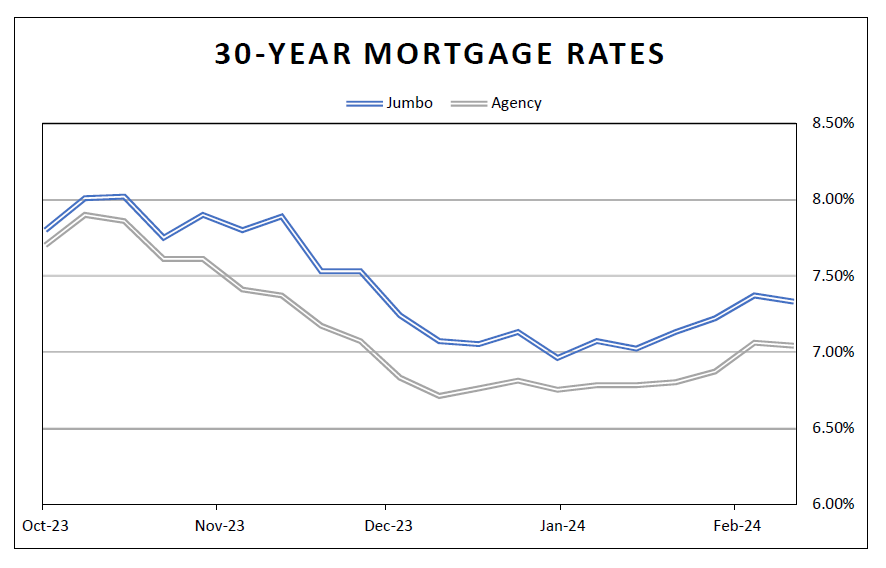

For most non-bank originators, finding liquidity for jumbo loans has been difficult since the onset of the pandemic. Recently, Mortgage News Daily reported the jumbo market share shrank from 12.2% in Q3 of 2023 to just 10.6% in Q4 with the full year 2023 contracting to 12.0% down from 17.8% in 2022. With jumbo 30-year fixed rates consistently higher than their agency counterparts, the jumbo sector is looking historically cheap on a loss adjusted yield basis but still not cheap enough to abstract new capital to the sector.

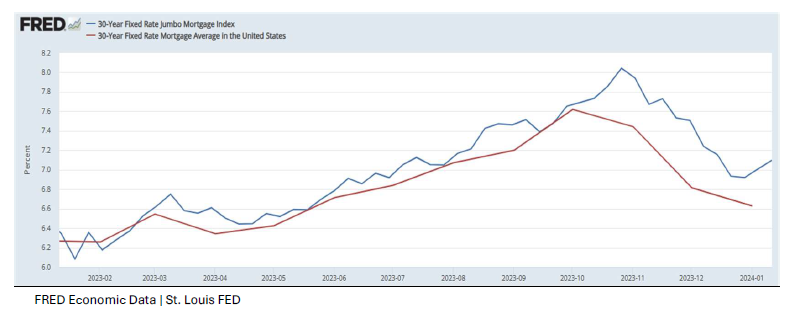

The chart below shows the Bankrate 30-year jumbo rate in blue and MBA’s weekly 30-year fixed rates in green over the last four months.

3 reasons why liquidity has waned:

Limited liquidity provided by bank porfolios given recent capital, deposit, and balance sheet issues. The securitization bid now dominates execution which is typically wider than the portfolio bid.

The inverted yield curve (high fed funds rates) means there is minimal to negative carry for buyers accumulating for a securitization exit. Typically, carry income provides a cushion for hedge costs and potential spread widening for the Investors. This is non-existent in the current market environment.

Other non-agency alternative loan types, like non-QM and closed end seconds, are more attractive assets for investors to securitize. Both have higher note rates and higher larger retained credit tranches. Jumbo loans will lose out to these other products for new money manager investments into the mortgage space.

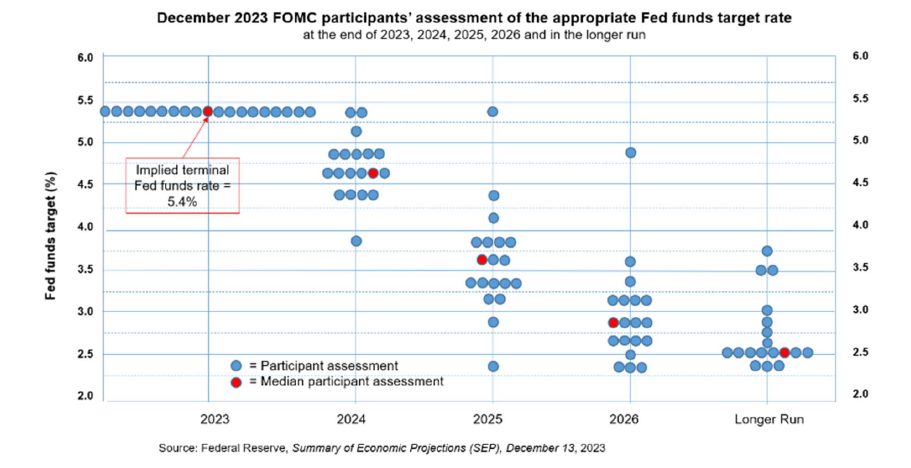

For jumbo loans to tighten back to note rates inside of agency, a few things need to happen. First, portfolio buyers need to emerge. With banks still largely on the sidelines, and many REITs unable to raise new capital due to share prices being below NAV, the market is looking for Insurance companies to fill the void. Insurance companies sold a record number of annuities in 2023, $360bln vs $311bln in 2022. Even with a modest allocation to mortgages, this could add much needed liquidity into the jumbo sector. Second, the treasury curve needs to go back to a positive slope. The Fed cung rates (assuming this happens in 2024) should have a positive impact on the securitization bid, bringing back positive carry into loan aggregation while also helping 2024 bank and REIT portfolio bids by healing balance sheets with higher portfolio asset prices. Given the projected Fed rate cuts (see the most recent dot plots below), this could happen towards the end of this year.

Filling the liquidity void with flow transactions.

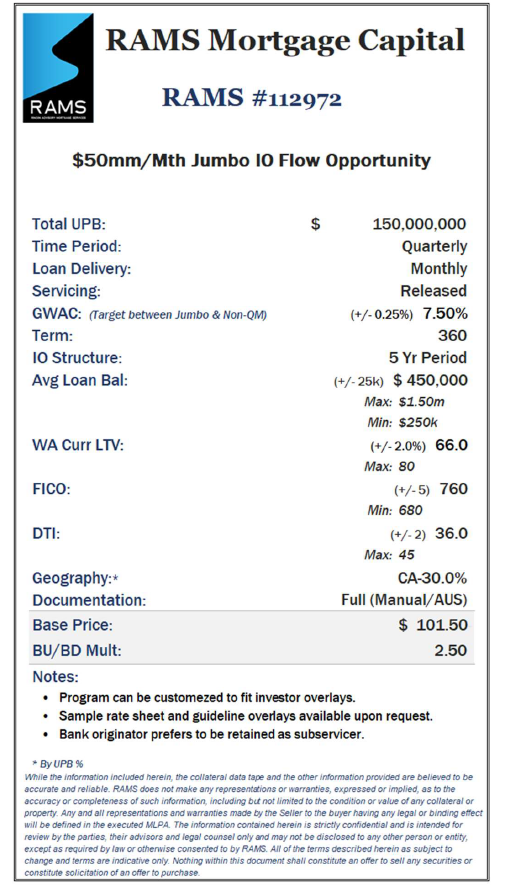

Both buyers and sellers widely adopted forward flow transactions for non-QM loans in 2022 in the face of diminishing liquidity. We think forward flow transactions can help fill the liquidity void in the jumbo sector as well. From the originator perspective, locking in flow execution allows for the start-up of loan programs or expansion of existing programs while locking in consistent pricing. For investors, it enables them to secure volume that matches specific risk tolerances by loan type. Each flow transaction is custom tailored to match the originator’s volume and credit characteristics with the investor’s needs at both the loan and pool level. We have sellers across a wide array of product types including non-QM, jumbo, agency NOO and fix & flip. Below is one example of a current opportunity for prime jumbo IO loans. If you have interest in exploring flow transactions as either a buyer or seller, please contact your RAMS representative.

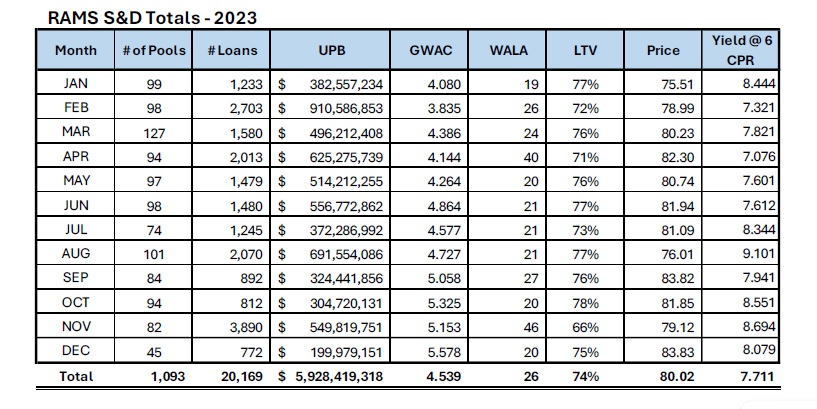

Scratch & Dent continues to be one of our most active sectors by number of offerings, so we thought both buyers and sellers would benefit from an in-depth look into the current structure of the market. Attracted by deep discounts, the availability of supply, and the lack of supply in other products, institutional investor interest increased dramatically in Scratch & Dent loans over the last year. Marketing close to $6bln of Scratch and Dent loans during this time, loss adjusted yields averaged 408bps over the 10yr treasury with prices hovering around 80%. The positive convexity of deeply discounted loans combined with the low dollar price limited the variability of returns from both a rate and credit perspective for investors. As we move into 2024, let’s take a look at what that may mean for the sector going forward.

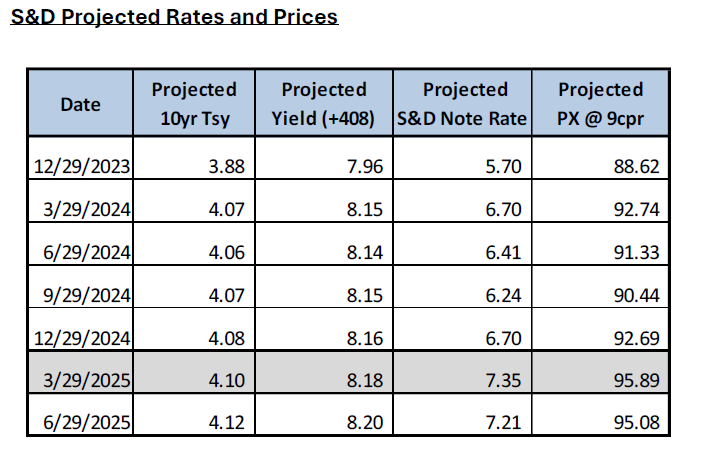

As we project what the S&D sector may look like, it’s important to realize that S&D loan note rates sold typically lag market rates on average by about 18 months. As rates rose throughout 2022 and 2023, this left a wider than typical spread between coupon and bid yields. The table below projects what S&D coupons may be available going forward based on the FHLMC 30yr survey rate with a 6- quarter lag while also projecting where investors will be bidding S&D assuming a fixed spread of 408bps over the 10yr treasury. The result is, by the end of Q1 2025, the spread between projected bid yield and S&D note rates compress to 83 bps with corresponding S&D pricing increasing into the mid-90s. This is simply due to higher production coupons making their way into S&D sales.

Conclusion:

For S&D buyers, be prepared for higher prices simply as a result of higher note rate loans coming to market in 2024. If buying loans in the 80s is a major part of your investment thesis, make sure to buy the lower note rate loans when you see them.

For S&D sellers, if you have low notes rate loans, now is a good time to sell into strong investor demand. The key drivers of price for deep out of the money note rate S&D loans is both a buyer’s CPR and yield assumption. Both are unlikely to change in the near term due to the flat forward curve and the out of the money note rates. Even in a rates down scenario, many of these assets won’t get the benefit of running faster speeds on discounted loans, so they typically underperform price expectations of sellers. Waiting to sell S&D only increases the opportunity cost of holding negative carry assets on the books while taking on more rate volatility risk that can be expensive to hedge. If you typically do not hedge your S&D position, the price action of the last few years should help persuade you.

Should you need any help knowing the value of your specific S&D portfolio or any other loan or MSR type, RAMS is offering whole loan mortgage value on services. We have built a database from the millions of bids observed in the past several years, across every type of mortgage imaginable (we even sold a butterfly farm loan last week!). The combination of our dataset, robust cash flow modeling and state of the art analytics allows us to provide a true mark to market price. Please call for more specifics. We hope this information helps you navigate the S&D sector in 2024 and beyond.

Congratulations! We have made it through another tumultuous year in the mortgage market. While 2023 had its share of difficult moments, we are happy to see it end on a positive note with the trajectory of lower mortgage rates giving us all something to hope for – the prospect of higher volumes in 2024.

We have come a long way in the last 12 months to get to where we are today. Recall, we started 2023 with just about every economist predicting a 2023 recession. We lived through the early March – Silicon Valley, First Republic and Signature Bank failures while collectively holding our breath to see if more banks would go down spreading chaos into our space, as we endured 100bps of Fed Funds Rate increases the first half of the year to see the Fed pivot in Q4, leading to trending lower mortgage rates at year end.

Even with the potential trajectory of lower rates, we are starting 2024 with the same liquidity constraints we saw in 2023. Most notably, bank secondary market activity remains limited. Bank purchase volume for RAMS dropped by 65% from 2022 levels. Aggregator, bank, and warehouse bank consolidation within the mortgage space is creating a difficult operating environment for many smaller originators relying on larger firms for takeouts or financing.

As we moved through 2023, what the market lost in bank portfolio liquidity, it picked up in credit focused private capital buyers. This is evidenced specifically in the S&D sector where loss adjusted yields tightened by 50 bps during 2023 while jumbos widened by 55 bps. Other more credit sensitive products outperformed as well with non-QM and DSCR outperforming jumbos by 35bps. The RAMS Whole Loan Pricing Report (see below) aggregates each quarter, across a myriad of loan types, tens of thousands of our bid observations. If you would like to be on the distribution list for this quarterly report, please contact your sales representative.

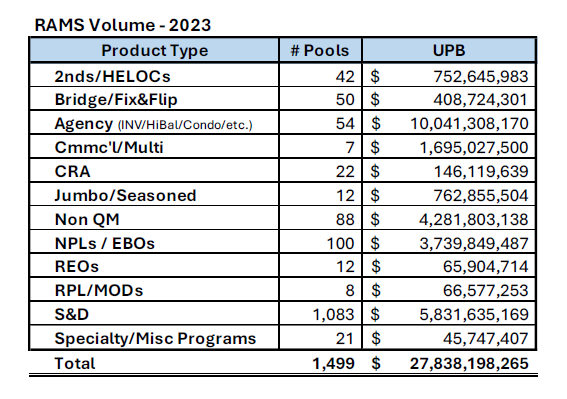

RAMS bid volume in 2023 was a robust 1,499 pools for $27.8 billion UPB despite total mortgage originations being down 27% from 2022 and 58% from 2021 levels. Details of our market volume are provided in the table below. The amount and variety of product types we trade in give us unique insight into current market dynamics and pricing. To that end, should you have any questions regarding where your specific loans would trade or need financial statement loan evaluations, RAMS offers whole loan mortgage valuation services. We would love the opportunity to earn your evaluation business.

Scratch & Dent “S&D”

S&D volume declined by 22% in 2023 in line with the decline in mortgage origination volume. In 2023, we did see the WALA increase on pools bid and a higher percentage of loans trade as pricing went from the 70s to 80s as that market tightened. Even with this decrease in S&D volume, RAMS still marketed more than 1,000 pools for $5.9 billion to maintain its leadership role in this sector. Adjusting for specific loan characteristics, S&D pricing remained consistent throughout the year in terms of yield, and tightened in spread, as new buyers entered the market. The positive convexity return profile of deep discount mortgage loans remains an investor favorite, and in 2024, the typical S&D loan profile should continue to trade at discounts albeit with continuing high demand.

Jumbo

As rates rose and the banking crisis unfolded in Q1 of 2023, the bank portfolio selling we anticipated did not materialize. The Fed opened their emergency term funding program to Treasuries and MBS and provided liquidity, lending on underwater securities at par. This alleviated capital requirements and balance sheet pressures, which enabled most banks to hold underwater jumbo loans versus selling at discounts. While still facing liquidity constraints, in 2024, we have already marketed multiple (with more in the pipeline) portfolios from banks who are now prepared to sell at discounts to par. This is a trend that we see continuing throughout the year.

On the jumbo buy side, REITs and Wall Street aggregators emerged as the dominant liquidity providers in 2023 as this sector widened throughout the year. Jumbo spreads are typically a direct reflection of the health of bank portfolios and the lack of bank activity impacted the relationship between conforming and jumbo rates creating room for a securitization arb. We saw new jumbo production rates widen significantly versus agency rates in 2023. Given the overall superior credit quality of jumbo loans, this was a surprise dynamic that leaves jumbo looking cheap to agency loans on a risk adjusted basis, and when banks are able (or willing) to buy again, we expect this will be the first sector they look to for residential mortgage assets leading to a reversal of this trend and spread tightening in 2024.

Non-QM & DSCR

Non-QM and DSCR loan sale volumes were hit hard in 2023 (see 2023 vs. 2022 comparison below). When the bank bid eroded in 2022, non-QM originators aggressively pursued long-term flow partnerships directly with end investors or transitioned into selling best eorts to aggregators for liquidity on generic product with securitization being the end result. This dynamic reduced loans available for bulk buyers which resulted in spread tightening in the sector as demand outpaced supply, a trend we expect to continue in 2024. RAMS specifically had success placing ITIN, Foreign National, and CDFI non-QM loans directly to end investors as replacement for generic bank statement, or DSCR, non-QM loans. As liquidity continues to come back into the loan space, we should see a reversal back towards originators increasing bulk sales to help mortgage originators obtain best execution and allow investors to aggregate enough volume in bulk for securitization.

Closed End Seconds “CES” & Home Equity Lines of Credit “HELOCs”

The second lien space was a bright spot in 2023 with new aggregators stepping in to fill the void left by banks and credit unions who left the space in 2022. We are seeing current production agency closed end second lien pools trading in the 105s (mid 8% yield at 15cpr) thanks to the securitization arb, and non-QM Second Liens trading 2-3 points lower. RAMS pool #112850 is the most recent example of an agency seconds pool that traded mid 105s servicing retained while RAMS pool #112843 is the most recent non-QM second lien pool that traded mid 103s released. We expect closed end seconds to be a 2024 bright spot for both originators and investors in terms of supply as more originators focus on the product. Hedging of second liens is more straight forward given the relatively shorter duration and with the deep investor pool, originators feel comfortable aggregating and selling in bulk transactions to obtain best-execution. This is a trend we expect to leak over into other credit sensitive, higher yielding, loan products like non-QM and bridge loans as liquidity comes back to the market and originators become more comfortable hedging in these sectors.

The HELOC market is historically dominated by banks and credit unions. With credit unions facing similar risk capital, balance sheet and deposit issues to their bank counterparts, the portfolio bid has yet to materialize. One 2023 bright spot for HELOCS is they can now be securitized thanks to a new structure that manages subsequent draws from the issuing trust administrator. Liquidity outside of the aggregators remains challenging especially for small pools or any loans not specifically originated.

GNMA EBOs

Our volume (in UPB) of GNMA EBO sales remained consistent at $3.3 billion in 2023 and in 2022, however, down from $7.8 billion in 2021 when EBOs traded at a premium. We are beginning 2024 with FHA EBO’s yielding mid 6% with VA and USDA EBOs trading wider in the low to mid 7% and expect volume in this sector to pick up in 2024. Pricing for 90-day delinquent FHA loans in Q4 2023 was approximately 1 to 1.5 points back of TBA plus refund of interest, escrow, and recoverable corporate advances. GNMA EBO sales volume is driven by a combination of (i) cumulative 60+ delinquency compared to maximum allowable GNMA levels, (ii) cost of carry for advances, especially in lower prepayment rate environments, and (iii) the re-delivery price for re-pooled loans. In general, 3% interest rate government loans were cheaper to retain in securities, but 6%+ interest rate government loans are good GNMA EBO targets and buyout should be evaluated.

In November 2023, the VA asked mortgage servicers to pause foreclosures for 6 months through May 31, 2024 and extended the COVID-19 Refund Modification Program. This action has left questions for the market and price discovery of VA EBOs has been limited as most EBO trades have involved FHA loans. This is interesting because pricing for newly originated FHA and VA loans was similar in Q4 2023. GNMA EBO Trades most often start with an evaluation, prior to buying subject loans out of agency MBS pools.

Bridge, Construction, Fix & Flip

In 2023, we saw aggregators within the bridge, construction, and fix & flip space exit the market making it advantageous for originators to align themselves directly with end buyers via vertical partnerships. The larger originators in these vertical partnerships are selling pass through rates in the 9.00% to 10.50% range. Smaller originators are selling the full coupon at par, or at slight discounts to par servicing released. With regional banks pulling back from portfolio lending in this space, we see an opportunity for outsized returns for investors who enable originators to maintain their

NPL

The NPL market continues to be active with a wide range of buyers who provide liquidity from a single DQ loan to larger NPL pools such as RAMS oering #112637 where we had 22 bids. We see fairly consistent pricing for NPLs with loss adjusted yields in the high single digits to low double digits depending on pool size, collateral characteristics, and geography. We ended 2023 seeing an increase in NPL loans out for bid with this trend continuing as we enter 2024.

As of late, especially on homes worth $1MM or more, we are seeing evictions continue to be a challenge. This issue is not unique to New York City or South Florida. We also have observed issues involving extended eviction situations in California, Illinois, New Jersey, Massachusetts, Connecticut, and Rhode Island. We anticipate deed in lieu of foreclosure or “cash for keys” will increasingly become the preferred resolution approach even though it is more expensive in the short term.

An observation worth noting is we’ve recently seen NY NPLs trading at lower prices due to a combination of factors including hard to project recovery timelines, higher carrying costs, and lower net recoveries. Moreover, the Foreclosure Abuse Prevention Act (“FAPA”) enacted in December 2022 added more uncertainty into the NY foreclosure process. The retroactive nature of this legislation is keeping NY courts from widely adopting this legislation and we are not aware of this impacting NY NPLs at the moment. There continues to be a select group of NY NPL buyers comfortable with the aforementioned property and legal related risks so while constrained, there is still liquidity for NY NPLs. The open question for the NPL market is will other states follow NY’s lead and enact similar laws to the detriment of NPL investors and housing prices.

We Thank You

2024 is shaping up to be an exciting year here at RAMS Mortgage Capital with new hires, and increased communication all to enhance capabilities, expand oerings, and better serve our existing and prospective clients. The most exciting new service added is our whole loan and mortgage servicing rights evaluation business. We have built a database from the literally millions of bids observed on the nearly 600 thousand loans we have marketed in the past several years, across every type of mortgage imaginable. The combination of our dataset and robust cash flow modeling and analytics sets us apart from other service providers because we can provide a true mark to market price. Couple this with a suite of custom reports and transparency of assumptions and variables and you will see why we are so excited about this new business.

To find out more please visit our website at (RAMS). Thank you for reading and we hope you have a great 2024.

It’s late Q3 2023. Do you have a plan for valuing and managing your whole loan portfolio? As a sector, depositories are the largest non-government owners of MBS and mortgage whole loans, and higher interest rates have put most mortgages originated before 2022 at a market price discount. But this doesn’t mean that banks’ best course is to sit still until prices come back to par. Strategic repositioning out of some old low-rate loans and into new higher-yielding assets in 2023 can enhance year-end balance sheets and increase net interest margins in 2024 and beyond.

Institutions that want the option to make strategic reallocations before year-end should start the evaluation process now. The first step is a careful assessment of where loans trade in today’s market. RAMS, a leader in whole loan trading, is uniquely positioned to provide accurate pricing, state-of-the-art analytics, and market insight to bank portfolio managers.

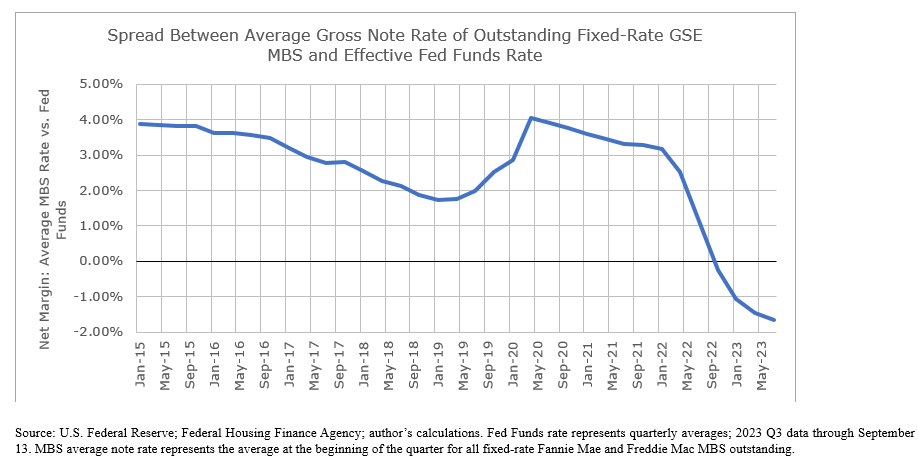

For banks, the problem goes beyond unrealized capital losses. Thanks to the Federal Reserve’s relentless increases in short-term rates, many institutions now face weak or negative net interest income on their mortgage loan portfolios. The pressures on interest margins are illustrated by the chart below, which tracks the spread between the average gross note rate of outstanding loans in GSE (Fannie and Freddie) fixed-rate MBS and the effective Fed Funds rate from 2015 to through 2023 Q3.

Source: U.S. Federal Reserve; Federal Housing Finance Agency; author’s calculations. Fed Funds rate represents quarterly averages; 2023 Q3 data through September 13. MBS average note rate represents the average at the beginning of the quarter for all fixed-rate Fannie Mae and Freddie Mac MBS outstanding.

As the chart shows, the average mortgage rate-Fed Funds spread has fallen by a stunning 500 bps over the past two years. This is the crux of the problem for banks’ net interest margins. While the tightening cycle may be near its end, it’s quite possible that the Fed will hold short rates at their current high levels for an extended period to wring inflation out of the system. That would subject owners of low-rate mortgage loans to years of weak net interest margins, before seeing real improvement.

For banks, the trade-off in any sale of underwater assets is taking short-term pain to achieve longer-term gains. The pain: a realized loss. The gains: improved future net interest margins and a balance sheet that shows fewer unrealized losses.

The equity market is painfully aware of this issue and can see the size of the unrealized losses. Every institution’s situation is unique. But with so many bank stocks trading poorly, it can be argued that this is precisely the time to attack the problem and begin the cleanup process. Looking ahead equity investors may look for improvements in net interest margin as a key marker of superior performance. In addition, demonstrating the ability to move or reduce the loan portfolio may allay concerns about shrinking deposits.

Strategic sales of low-rate loans to reposition into higher-yielding assets can launch a bank toward higher future net interest margin. The first step in this process is an accurate portfolio valuation assessment, which should provide the following information:

• Real-time, loan-level market prices that accurately pinpoint where assets trade today. • Risk assessments, with particular focus on interest rate risk (duration and convexity). • Principal runoff projections.

This evaluation helps banks achieve two objectives:

• Assess where they can achieve the best bang for the buck – gain-to-pain ratio – via portfolio reallocations in 2023. • For loans that don’t currently make sense to sell, establish a future action plan to implement when market levels make their sale more attractive.

Liquidity in the whole loan space is strong, right now. The market’s not frozen; the shock of higher rates has worn off, and a wide range of assets trade regularly in well-defined price corridors. That said, it’s rarely good to be a “before year-end” seller in the last few weeks of the year. Now is the time for banks who want the option to reallocate assets in 2023 to begin the strategic evaluation process. Don’t wait till Thanksgiving.

With mortgage rates high and production supply down if you have needs for CRA eligible loans for lending credit you don’t want to wait till Thanksgiving either. RAMS has a national pipeline of CRA eligible in the billions every day. Please let us know if we can help you in your search for these low to moderate income mortgage loans.

RAMS Mortgage Capital is a mortgage trading business that provides financial institutions and investors with solutions to increase revenue and profitability while managing risk and volatility. RAMS is one of the most active loan broker-dealers in the country, trading the full spectrum of loan products. Whether you have a single loan or a multibillion-dollar pool, RAMS will ensure the best execution from bid to settlement.

Here’s to the end of a difficult and challenging 2022. December 31st may be just a date on the calendar, but Jan 1st is that magical day where we all get to reset our P&Ls to zero. They say a person can drown in a lake with an average depth of 2 feet. We think about this saying when we review 2022 and average it with the previous 3 years.

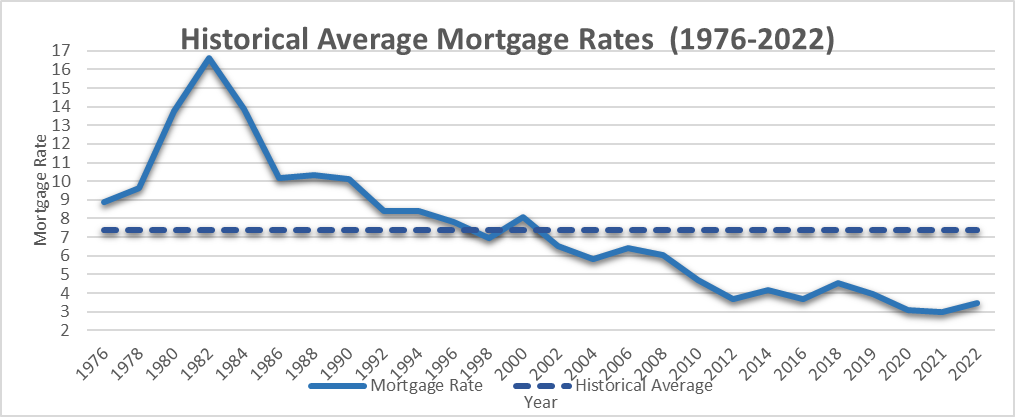

Before we discuss specific sectors, we thought we’d start with a look back at historical mortgage rates to illustrate what an unprecedented 3 -year period (2019 – 2021) was of exceptionally low rates and easy money. Below is a graph of the average mortgage rate going back to 1976. The average mortgage rate over the past forty odd years has been 7.38%, 4.53% over 20 years and 3.365% the last three years.

2022 marked the first extended period of rising rates and waning liquidity that many market participants have ever experienced.

The Federal Reserve hiked rates seven times in 2022: 25bps in March. 50bps in May. 75bps in June, July, September, and November, and 50bps in December. The Fed has done what it said it would do all along, they also said they aren’t done raising rates and would not be easing in 2023.

Liquidity has been limited as investors finished out the year and closed the books for 2022. There has been an exodus of bank deposits into higher yielding fixed income assets, and a flight to quality and higher yields available in shorter term treasuries with current yields of >5% and >4%, on 1yr and 2yr T-bills, respectively. Investable dollars were constrained in Q4 of 2022 as prepayments slowed. These projected dollars have not yet returned back into the investment market. Moreover, we have reorganizations taking place at some of Wall Street’s largest investment banks and major mortgage players. The MBA has forecasted origination volume will decline to between $1.5 to $2 trillion after having been more than $4 trillion in each of 2020 and 2021 and just under $2.5 trillion in 2022. The treasury is no longer buying new issue MBS, (they were buying~40% of all TBA mortgages issued), but this hasn’t hit market spreads due to low prepays. Primary mortgage spreads over the past 10 years, have averaged ~75 to 80 bps, with the current spread near 200-bps. This means if the yields on the 10-year Treasury note remain in and around 4%, and spreads revert towards the 10-year average, then mortgage rates should drop into the 5% range.

We see this as a buyer’s market with the highest yields we’ve seen in years. There continues to be a battle for the cheapest assets as investors are comparing yields across alternative asset classes. Conversely, new production with high coupons struggle to obtain premiums given a potential market rally in 2023, which could lead to high prepayments and the vaporizing of premium prices paid on these newer higher coupons.

SCRATCH & DENT “S&D”

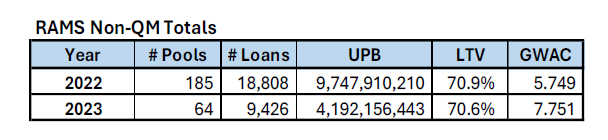

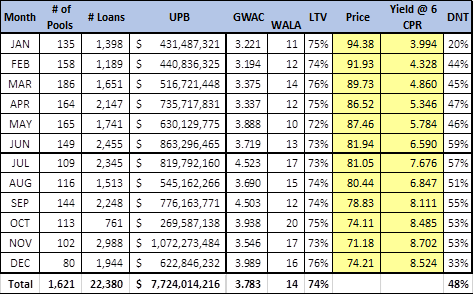

2022 was another record year for agency and aggregator putbacks as loans with some sort of defect rendered the loans undeliverable. RAMS bid 1,621 pools with 22,380 loans for $7,724,014,216 in 2022.

Originators, who decided not to sell their S&D loans last year due to pricing in the 60’s for loans with interest rates between 2% and 4%, expect pricing to go up as if the New Year included a magical “switch” where interest rates would stabilize and start to decline in short order resulting in higher loan prices. There is usually a pickup in pricing in Q1 as buyers have fresh budgets and look to buy loans, but we are not going back to 90’s pricing on lower rate loans anytime soon.

As shown on the Table below, pricing on S&D loans in 2022 began in the low to mid 90s, but due to the continued market sell off and coupons in the mid 3s, we saw pricing decline down to the low 70s and even upper 60s on certain pools.

As levered buyers moved to the sidelines, an influx of banks and unlevered buyers entered the market with yields in the high single digits to as high as ~9.5%. We are often asked why prices don’t rise when TBA MBS prices rally. The answer is, since S&D loans aren’t deliverable into the TBA market, yields more closely reflect investment yields in the credit sensitive side of the market correlated to the Private Label Securities market (PLS). These low coupon loans, with very slow prepayment assumptions, create long durations that are unattractive to investors. We aren’t believers in the current prepayment assumptions being used in the market, because life happens – people move for jobs and other reasons, a need for more space, divorce, and old age. If these loans never prepaid, and the borrower made their 360th and final payment, you’d be earning a high single digit return with tremendous potential upside if that borrower pays prior to maturity.

We’ve seen a huge pickup in “Did Not Trade” (DNTs) although the Fed says continued rate hikes are ahead. Nearly half (48%) of these pools did not trade due to sellers’ unwillingness to accept current market price levels and/or hoping for prices to improve in 2023. In years 2019 thru 2021 the number of DNT’s was less than 30%. In 2022, we saw a bifurcation between large and small originators in terms of their respective willingness to sell lower rate S&D loans and absorb the related loss on sale. We saw some very large S&D trades completed late in 2022 by large originators, while small originators held onto more S&D loans than they sold.

Most S&D loans are over a year seasoned and we anticipate another 6 to 10 months of heavy volume before we see this start to taper off. In its most recent filings Fannie had $939mm (as of 9/30/22) in outstanding loan-repurchase requests and Freddie had $1.3BB (as of 12/31/21) with originators stating requests had picked up throughout 2022.

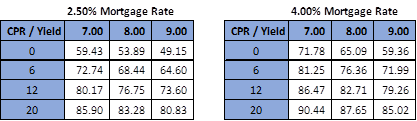

Below is a table showing the price sensitivity of changing yields and prepayment speeds assuming 2.5% and 4.00% mortgage loans

What this shows, is even a 100-bps tightening in required yields by investors only improves price by 3 to 4 points. With the marginal upside and negative carry we encourage originators to let the asset managers try to make sense of these lower coupons.

NON-QM

It was a tough year for Non-QM & DSCR originators as they struggled to keep pace with rapidly rising rates and widening spreads. With liquidity waning and the private label securitization (PLS) market in hibernation, we saw warehouse lenders apply pressure to their clients. With the restructuring of one of the largest lenders, and others announcing they may be stepping away from Non-QM financing, advance rates and dwell times are being re-evaluated and re-marked for both current coupon and out of the money production.

There is a backlog of pools ready for securitization and spreads recently have tightened. OCT/NOV “AAA” spreads widened out to ~ +290. A couple of deals were quickly placed at year end at around +220 after not much activity in new deal flow after Thanksgiving. The first deal of 2023 saw AAAs go subject at +175.

The trend for Non-QM production is down. RAMS bid on 250 pools for $12 billion. Consumer Non-QM is currently sub 8% with DSCRs in the mid to high 8%. ITINs and Foreign National yields are back of those more liquid products by a point or two.

Please see table below for Non-QM and DSCR activity by month:

NPLs & EBOs & RPLs

2022 saw a slowdown in NPLs and EBOs as serious DQs shrunk to 1.2% vs 2.4% in 2021 and G2 TBAs lost nearly fifteen points over the year. RAMS marketed 80 pools with 38,592 loans for $5,497,020,296.

GNMA EBOs

When many GNMA EBO loan buyers think of the term “EBO” or “Early Buy Out,” they envision loans either still in a GNMA Security where the Seller is planning to execute a concurrent buyout / sale transaction, or the GNMA EBOs will be repurchased and held for a very brief period by Seller before the loans are sold. In the last two quarters of 2022 (and beginning of 2023), the largest GNMA EBO trades involved the sale of loans repurchased over a year ago. We will see if this trend continues or if Sellers need to execute GNMA EBO trades to help their delinquency rates get back to compliant levels and/or fund advances.

There is no question the pricing of GNMA EBOs is directly impacted by GNMA II Securities pricing. Since we are performing a GNMA EBO evaluation and “sell or hold” analysis for multiple clients on a quarterly basis, we track GNMA II Securities prices and their corresponding impact on GNMA EBO prices very closely.

The great days of 2021 when GNMA EBOs were sold for par, or over par, plus refund of all advances are gone and may not come back for years if ever again. GNMA EBOs are not a profit generator today. Loss Mitigation is the name of the game now. We are big proponents of having a GNMA EBO strategy, so much so that we provide free GNMA EBO Analysis and will help you plan and execute your strategy. Just send us a tape for review and discussion.

NPLs

Conventional NPL pricing for loans with 2%, 3%, and 4% interest rates in the high 50’s to high 60’s (as a percentage of UPB) range in Q4 2022. NPL Buyers had to account for the possibility of borrowers reperforming and getting “stuck” with a long duration, low coupon, asset. The good news for these NPL Buyers is buying NPLs at these levels provides a relatively low “effective LTV” (calculated as actual LTV * purchase price) even if the actual LTV is around 90%. This gives NPL Buyers a lot of cushion in dealing with continued falling home prices. This also provides NPL Buyers with some runway to workout settlements with borrowers before we get close to any kind of property value issue.

We currently see NPLs trading to unlevered yields in the 9%+/–range and this has been steady through Q4 2022.

Odd lot, or small, pools of government insured loans continue to be a bargain, in our opinion, especially FHA insured and lower ltv VA insured loans. On small pools of government insured loans, the NPL Buyer may be asked to refund recoverable escrow advances, but we have not seen many trades (although there are a small amount) where a Buyer will refund recoverable corporate advances. We do not see Buyers refunding interest advances on these smaller trades, so there is a lot of upside if a Buyer can recover advances.

Q3 and Q4 2022 pricing of residential NPLs were heavily impacted by the “risk” of reperformance. The goal of buying NPLs for several decades prior to this year was to get borrowers to reperform and then sell the reperforming loans, into the PLS market. This is very different today. An NPL pool with a high likelihood of reperformance combined with interest rates of 2% to 3.5% can price in the 60’s as a percentage of UPB with a price in the 40’s as a percentage of property value. We think this may be a good time to rethink the RPL sector. These used to be non-performing borrowers from the last Great Financial Crisis that were brought current through some type of modification, typically lowering the coupon, and extending the maturity. Aren’t these just seasoned loans now?

We are also starting to see, for the first time in a while, property valuation variances of opinion between Seller appraisals or BPOs and Buyer BPOs. There are multiple reasons for the variances, and no two evaluations are the same, but the one issue we see more often than others is the use of bad comps, especially on jumbo properties. Sometimes comps are hard to obtain when pricing a property that is much bigger and nicer than others in the area, so the appraiser uses comps from a very high-end neighborhood to comp a property in an average area. We saw one example where the variance was over $3MM on a $7.5MM property.

Many NPL buyers expect 2023 to be full of opportunities as borrowers deal with higher costs of living and lower home values. For an early warning, one area to keep an eye on, is FHA loans, where >80% of FHA purchase volume is first-time homebuyers. According to 2021 HMDA [Home Mortgage Disclosure Act] data, the median income of FHA borrowers is $65,000 per year, compared to $85,000 for VA and $105,000 for conventional borrowers. Lower income families, having just purchased their first home, tend to have limited savings, and stretched budgets, with little ability to adjust to higher inflation, declining property values, and rising unemployment if there is a recession later this year.

We will address Bridge, Fix & Flip, Jumbo, and Specialty Loan Programs in our next update. These segments of the market faced their own unique challenges in 2022.

We like to end our updates with something positive in spite of 2022. We could have gone with the old standby from President Franklin D. Roosevelt’s 1933 Inauguration Speech, “You have nothing to fear but fear itself.” Instead, in honor of the upcoming Martin Luther King, Jr. holiday we will finish with his quote, “Only in the darkness can you see the stars.”

Where are we in whole loan land? Where are we going?

We can answer the first question – Prices are lower, yields are trending higher, and liquidity comes at a premium. The second question generates more questions than answers.

TBA prices have dropped more than ten points since the beginning of the year however non-TBA eligible loans execute into a much less liquid market.

Financing costs have gone up (if financing is available at all) and another Fed interest rate hike is coming next week with an expected raise of at least 75 basis points. The Fed is in the midst of its quantitative tightening plan and 09.14.22 was the last day of MBS purchasing by the Fed. This coupled with out of the money coupons is driving scratch & dent prices lower. We know these lower coupon putbacks from the agencies will continue well into next year but where are scratch & dent prices now?

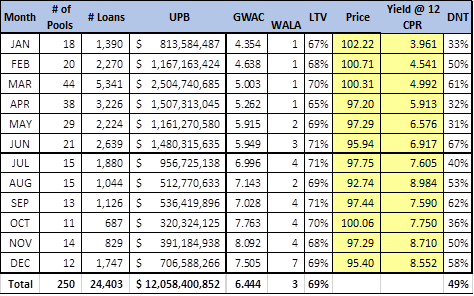

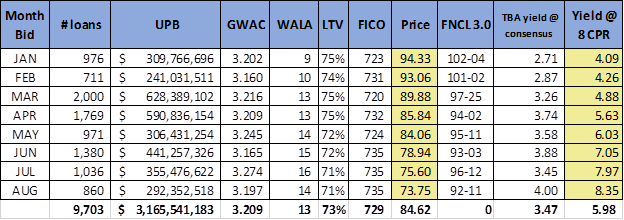

From January to August 2022, we have marketed over 1,250 pools with an aggregate UPB around $5.5BB. The bulk of these pools contained loans originally destined for agency execution, so the loan characteristics are similar to collateral in the TBA market: Low 700s FICO, Low 70s LTVs, and Low/Mid 40s DTI’s. Coupons ranged from mid 1’s% to 9% and prices from high 50s to 102+. To track pricing, we compressed our subset to include only pools with coupons between 2.75% and 3.50%. For this subset, there were 589 pools with a UPB of $3.2BB and a 3.209 GWAC. Please see Table 1 below for a comparison of average price for S&D vs. FNCL 3.0 TBAs, along with their corresponding yield at dealer consensus prepayment speeds, as well as the whole loan equivalent yield at an 8 CPR.

Table 1

Discount rate is the most sensitive pricing variable for these out of the money coupons. This is followed by prepayment speed, where a lower prepayment speed not only lowers price, but also extends duration to a level viewed as unattractive by many institutional investors. We have heard of bidders using a zero CPR for the lowest coupons. Do you know of anyone that has ever made a 360th payment? Life happens, and loans payoff for lots of reasons unrelated to interest rates.

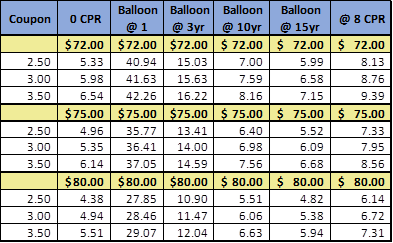

Table 2 below reflects the yield at different coupons using a zero CPR and balloon prepay at the end of years 1, 3, 10, and 15.

Table 2

We believe owning performing mortgages at 20+ point discounts to par is a solid strategy if you have patient capital.

RAMS is here to help firms get through these turbulent times.

We have marketed more than $200BB in REOs, NPLs, RPLs, agency eligible, scratch & dent and specialty loans. With all the pricing data gathered from trading, we are expanding our evaluation services! We are currently evaluating billions in UPB every week for clients including warehouse banks, hedge funds, accounting firms, banks, and most recently, originators choosing to hold loans requiring a mark for their annual audit. Let’s set up a call to discuss your evaluation requirements.

“In a time of turbulence and change, it is more true than ever that knowledge is power.” JFK

Things have been moving so fast we haven’t been able to get this market update out before today.

Primary rates beginning of the year to today:

Brutal second quarter for the mortgage market.

Today, origination pipelines are down considerably, margins are being squeezed, margin calls are commonplace, thousands of employees have been laid-off, volatility is spiking, funds are managing redemptions, trades have been repriced or failed, durations continue to extend and there is a buyers strike in the PLS market. As the saying goes, “Other than that Mrs. Lincoln, how was the play?”

The Fed wants to slow down inflation and intimated they could raise rates in the next seven meetings and have done so in 3 out of 3 with the most recent an unprecedented 75bps. Are we almost halfway there? Who knows, but the 10 year does not seem to want to break 3.00%

Where does all this leave us? Many mortgage bankers are shifting to best efforts from mandatory delivery, yields have hit a level I wish my stockbroker could achieve, and the whole loan market is flooded with opportunities we have not seen since 2010.

We have clearly transitioned from a sellers’ market to a buyers’ market. Levered buyers are on the sidelines and with buyer yield requirements increasing from 7% into the double digits. We’re at yields that have historically proven to work out well.

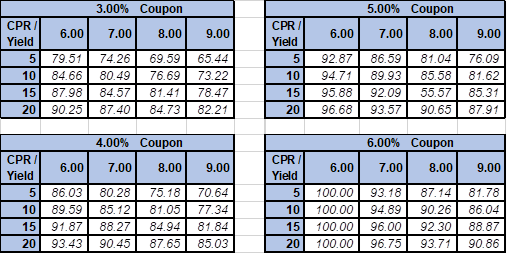

Below tables show the change in price at different fixed interest rates, prepayment (CPR) speeds and yields:

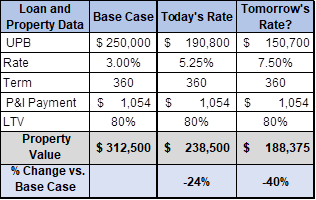

We constantly hear about rising rates impacting mortgage payments and/or that homeowners with 3% mortgages will never prepay.

Although rising rates will not change anything on a borrowers conforming 30-year fixed rate mortgage, the table below shows what could happen to future home prices when solving for a consistent mortgage payment:

We are not predicting a 40% decrease in home prices, but home affordability warrants consideration. We also think models are overestimating slower speeds. Regardless of rates, homeowners still pay off when they move up, move down, have babies, divorce, or just need cash. Furthermore, baby boomers are about to downsize in mass, and this will impact prepayment’s as well.

Non-QM

The Non-QM market has been in shambles, dragging everyone down together. Investors and aggregators have felt the pain caused by extended durations while originators struggle to right size current coupon and find any liquidity, in this fast-moving market.

The PLS market (execution of choice for this sector) is experiencing a buyers strike leading to wider spreads and much higher rates. We started 2022 with AAA spreads around +150 and the 10-year at 1.63% and now we are around +235 spread with a 2.90% 10-year. This combination of factors took the par coupon from 3.875% to where it feels like we have settled in around 7.00% and 7.375% for DSCR.

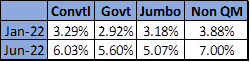

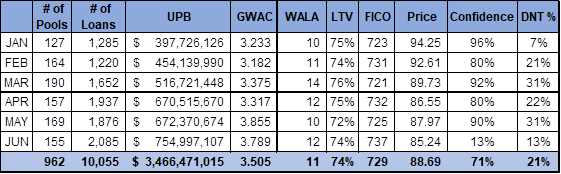

Below is a month-to-month snapshot of the Non-QM/DSCR market from January thru June 2022:

**Confidence Quotient is the percentage of sellers that have accepted RAMS’ bid or communicated to us what they are doing with the subject loans.

Scratch & Dent

In our view, the scratch & dent loan sector is currently pricing cheapest in the residential loan market. Levered buyers had dominated this part of the market. Yields for scratch & dent loans, using reasonable prepay speeds, are in the high single digits, unlevered, and well into the double digits if the borrower pays off early.

Pricing has been hit hard due to duration concerns and rates are lower than current market since the S&D sector is generally selling ~12-month-old production, once it has been put back to the originator. However, we believe investors are using overly conservative prepay assumptions (see highlighted statement above). Production is down significantly, and we believe yields will improve due to a supply scarcity once we get through this storm.

Many sellers are not ready to accept today’s lower price levels, but the current ebb and flow of liquidity allows investors to be more selective and targeted than in more orderly times.

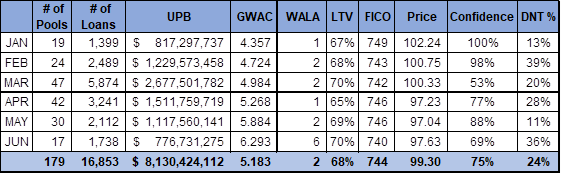

Below is a month-to-month snapshot of the S&D market from January thru June 2022:

**Confidence Quotient is the percentage of sellers that have accepted RAMS’ bid or communicated to us what they are doing with the subject loans.

Remember, this product was intended to go into agency MBS securities, so the average LTV and FICO is pretty consistent. What you will notice is the coupon is increasing while the price is decreasing. Color (aka pricing feedback) is what we are trying to share in this letter. Unfortunately, sellers are not quick to react in this sector due to the discounted prices and loss and/or view there may be other options. We appreciate, buyers investing their time and energy in bidding for loans, so we will continue to request color and feedback from sellers.

We currently have 81 pools with 1,165 loans and $390mm in UPB for the bid. Call us for offerings.

Jumbos

The Jumbo market has experienced some damage but not as severe as the Non-QM sector. There were some banks that could not get their PLS deals off in time before rates rose and spreads gapped out. Jumbo PLS issuance is dominated by Primary Broker Dealers. They can react quicker to volatile markets and are better positioned to hedge both the rate and spread risk while aggregating jumbo product. Many independent mortgage banks sell their jumbo on a best-efforts basis, so it limited the damage and hedge losses experienced by the larger aggregators and issuers.

A recent JP Morgan deal with a 3.0% coupon with senior AAA’s at 4-16/32 back of TBAs priced in the high 80s. We sold $100mm just inside of a 5.50% yield.

Bridge, Fix & Flip

This sector has taken a similar beating with a lack of liquidity (one recent PLS deal received no “indications of interest”) and a few originators have halted fundings.

As we have been touting, bridge loans offer a high return with much shorter duration (2yr terms in general). Prior to this run up in interest rates, bridge loans were typically sold at par with a passthrough rate of between 5.5% and 7.0% on a servicing retained basis. Today, that rate has risen to 8.5% or greater and loans are being sold on a servicing released basis.

If you are a residential non-performing loan buyer, you might want to consider buying performing bridge loans. Unlike a 30 year, 3% interest rate NPL, where there is material risk of the loans re-performing and the extension of a 3% yielding asset, bridge loans have short maturities, usually 2 years or less. If a performing bridge loan defaults, or does not pay-off at maturity, many have default interest rates that range between 18% and 25%. If you are adept at managing REO, you should be comfortable taking over a rehab project in the event of default because the resulting return, can be a much greater. This a great sector for investors limited by geography as you can pick the locations you like.

We currently have nine pools offered with properties located across the nation for >$200mm.

EBOs/NPLs

EBOs

This trade has run its course until/if delinquencies rise. Pricing has dropped alongside with G2 TBAs and lower reperformance projections. With the rise in primary rates, it is cheaper to finance these loans in the MBS security than to buy them out and finance them on a warehouse line.

NPLs

NPL sales are still not prevalent, and the lack of supply has helped this sector avoid the drubbing taken in other sectors, although we may have passed its peak pricing. We are watching closely how borrowers coming out of COVID forbearance plans are going to perform as this could increase supply – perhaps dramatically. We also know refinancing to avoid a pending default is much tougher now than just a few months ago.

NPLs are trading to a lower discount rate than used by consistent buyers of performing and re-performing loans. There are two primary reasons for this. First, buyers of NPLs are more confident about the duration of their investment assuming a foreclosure sale followed by REO liquidation outcome. Second, some investors have a maximum holding period of between 3 and 7 years. Therefore, investments with durations beyond the holding period require a projected exit price, which today is relatively low vs. 3 months ago.

Geography remains a major focus of NPL buyers. Southern states, especially Texas and Florida are preferred. New York, especially Southern New York, for many buyers is a non-starter. Many buyers still have 2004 to 2008 vintage NY NPLs in their portfolios and do not want to buy more. California, which not too long ago, was considered a relatively fast foreclosure state is becoming an issue for some buyers, especially buyers of super jumbo NPLs where borrowers have become adept at fighting eviction following foreclosure sale.

Interesting current market fact. Loans with comparable coupons and characteristics – one performing and one NPL. Which loan has a higher price as a % of UPB? The NPL.

Below are examples of recent trades reflecting this phenomenon:

Something to think about:

How many home buyers bought because of low rates with the sole intent of selling as home prices continued to rise. How many do not have a long-term view and will sell or go into foreclosure? We will see.

We leave you with this inspirational quote:

“You never know how strong you are until being strong is the only choice you have.” – Bob Marley

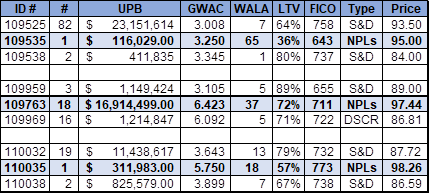

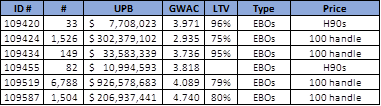

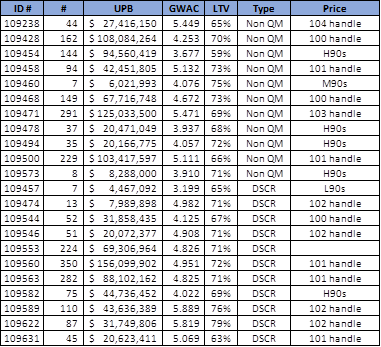

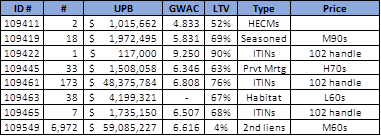

With all the market activity and volatility, it’s been difficult to get color out on the pools we’re marketing. Year to date, we’ve marketed 476 unique pools for $8.7BB. Below is color on 216 of those pools for ~$3.9BB. If you bid and are looking for more detailed color, please call. If you didn’t bid and are just receiving free color, you’re welcome.

Sellers as you can see below, we’ve been very active across all product sectors as well as CRA trading and arranging specialty programs for investment partners.

Thank you all. We appreciate your business.

6 EBO pools for roughly $1.5BB – most traded above par plus all advances

22 Non QM pools for $1.2BB – 11 were DSCR, 11 were consumer